The Markets (as of market close January 31, 2018)

Equities pulled back off of their record-setting gains at the end of January, but not enough to forestall a month of significant gains. January provided several noteworthy storylines for investors to consider. Unemployment remained low as the number of available job openings continues to recede, possibly signaling a push for higher wages, Fourth-quarter corporate earnings were relatively strong. The president's first State of the Union address preached optimism and called for bipartisan cooperation on major economic and international issues. The government shut down for a few days before approving a stopgap budget resolution through early February. Some American workers saw a modest bump in pay, courtesy of the Tax Cuts and Jobs Act legislation passed in December. And Janet Yellen's final meeting as chair of the Federal Reserve saw the Committee maintain interest rates at their year-end level.

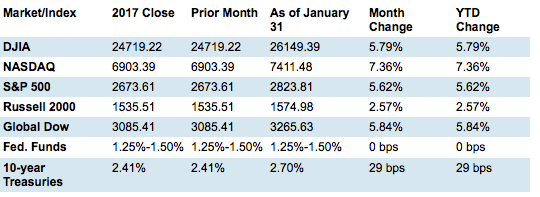

The month started on a strong note as the Dow soared past 2500, ultimately reaching 26000 mid-month. The S&P 500 closed the first week of January up 2.6% and continued to post positive weekly gains through the month, ultimately gaining over 5.5%. The tech-heavy Nasdaq picked up in 2018 where it left off in 2017, gaining 7.36% by the end of January. Both the Global Dow and the small caps of the Russell 2000 enjoyed positive monthly returns, closing up 5.84% and 2.57%, respectively.

By the close of trading on January 31, the price of crude oil (WTI) was $64.77 per barrel, up from the December 29 price of $60.10 per barrel. The national average retail regular gasoline price was $2.607 per gallon on January 29, up from the December 25, 2017, selling price of $2.472 and $0.311 more than a year ago. The price of gold increased by the end of January, closing at $1,348.50 on the last trading day of the month, up $43.40 from its price of $1,305.10 on December 29, 2017.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Month's Economic News

- Employment: Total employment rose by 148,000 in December following November's revised total of 252,00. Employment gains occurred in health care, construction, and manufacturing. The unemployment rate remained at 4.1%. The number of unemployed persons marginally declined by 40,000 to 6.576 million. The number of new entrants to the workforce increased by 116,000 in December. The labor participation rate remained unchanged at 62.7%. The employment-population ratio was unchanged at 60.1% in December but was up by 1.3 percentage point over the year. The average workweek for all employees remained at 34.5 hours in December. Average hourly earnings increased by $0.09 to $26.63. Over 2017, average hourly earnings have risen $0.65, or 2.5%.

-

FOMC/interest rates: The Federal Open Market Committee met for the first time in 2018 at the end of January, marking the last meeting chaired by Janet Yellen. By a unanimous vote, the Committee decided to leave the target federal funds rate range at 1.25%-1.50%. The Committee also selected Jerome H. Powell to serve as its chairman, effective February 3, 2018. Nothing from the latest meeting indicates a change from prior statements - economic activity is expected to continue to strengthen, with gains noted in employment, household spending, and business fixed investment. The Committee next meets in March.

-

GDP/budget:The first estimate of the fourth-quarter gross domestic product showed expansion at an annual rate of 2.6%, according to the Bureau of Economic Analysis. The third-quarter GDP grew at an annualized rate of 3.2%. Consumer spending rose 3.8%, with notable increases in durable goods spending (14.2%) and residential investment (11.6%). As to the government's budget, December's deficit was $23.2 billion, increasing the fiscal 2018 (October, November, and December) deficit to $225.0 billion - 7.2% higher than the deficit over the same period last year.

-

Inflation/consumer spending: Inflationary pressures continued to show continued upward momentum in October. The personal consumption expenditures (PCE) price index (a measure of what consumers pay for goods and services) ticked up 0.4% for December following a November gain of 0.6%. The core PCE price index (excluding energy and food) inched ahead 0.2% in December. Personal (pre-tax) income increased 0.4% and disposable personal (after-tax) income gained 0.3% from the prior month. Personal consumption expenditures (the value of the goods and services purchased by consumers) climbed 0.4% in December after jumping 0.8% the prior month.

-

The Consumer Price Index, which rose 0.4% in November, edged up only 0.1% in December. For 2017, consumer prices are up 2.1%, a mark that approaches the Fed's 2.0% target for inflation. Core prices, which exclude food and energy, increased 0.3% in December, and are up 1.8% for the year.

-

The Producer Price Index showed the prices companies receive for goods and services fell 0.1% in December- the first decline since August 2016. Year-over-year, producer prices have increased 2.6%. Prices less food and energy also dropped 0.1% for the month and closed 2017 up 2.3%.

-

Housing: The Home sales slowed in December. Total existing-home sales dropped 3.6% in December after climbing 5.6% the prior month. However, over the last 12 months, sales of existing homes increased 1.1%. The December median price for existing homes was $246,800, which is 5.8% higher than the December 2016 price. Inventory for existing homes fell 11.4% for the month, representing a 3.2-month supply. The Census Bureau's latest report reveals sales of new single-family homes also fell in December, declining 9.3% from November. Despite the December swoon, new home sales closed the year 14.1% above the December 2016 estimate. The median sales price of new houses sold in December was $335,400. The average sales price was $398,900. There were 295,000 houses for sale at the end of December, which represents a supply of 5.7 months at the current sales rate.

-

Manufacturing:Industrial production increased 0.9% in December, despite manufacturing output edging up only 0.1%. Industrial production rose 3.6% in 2017. Capacity utilization increased 2.0 percentage points to 77.9% in December. Mining output increased 1.6% for the month, and is up 11.5% from its year-earlier level. The index for utilities jumped 5.6% for December and 1.8% for 2017. New orders for manufactured durable goods jumped 2.9% in December following a 1.3% November gain. For the year, new durable goods orders increased 11.5%.

-

Imports and exports:The advance report on international trade in goods revealed that the trade gap increased in December from November, rising from $69.7 billion to &71.6 billion. Exports of goods for December jumped 2.7% following November's 3.3.% gain. Imports of goods climber 2.5% after rising 2.7% in November. Still, total imports ($209.2 billion) far exceeded exports ($137.6 billion). Prices for both imported and exported goods and services were weak in December. Import prices rose only 0.1% for the month, while export prices fell 0.1%. For the year, import prices increased 3.0%, while export prices advanced 2.6%.

-

International markets: Several advanced economies, including Germany, Japan, and South Korea, experienced higher-than-expected economic growth in the third quarter. Other countries, such as China, Brazil and South Africa, also posted third-quarter growth that exceeded expectations. Preliminary information on the fourth quarter is showing continued growth. As the U.S. dollar fades, the euro has increased in value, reaching a three-year high compared to the dollar. The European Central Bank kept its monetary policy intact in January, despite encouraging economic growth in the E.U. In China, growth in industrial profits slowed, which could continue through 2018.

- Consumer sentiment:Consumer confidence, as measured by The Conference Board Consumer Confidence Index®, increased in January after falling in December. The index increased to 125.4, up from 123.1 in December. According to the report, consumer expectations in the economy improved in January following a sharp decline the prior month.

|

Eye on the Month Ahead All Investors hope stocks continue to soar in February following January's impressive performance. The Federal Open Market Committee (FOMC) does not meet in February, so interest rates will remain unchanged through the month heading into March. Oil prices are expected to maintain their current prices during the month, while the U.S. dollar may sink further. |