The Markets (as of market close October 31, 2018)

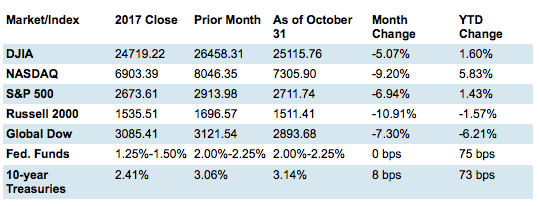

October truly was a scary month as stocks closed the month well below their end-of-September values. The tech-heavy Nasdaq lost over 9.0% by the end of October, while the small caps of the Russell 2000 fared even worse, losing almost 11.0%.

The S & P 500 fell close to 7.0% -- its largest largest monthly decline in over seven years. The Dow dropped 5.0%, and the Global Dow sank over 7.0%. A slide in internet stocks, coupled with investor concerns that global economic growth is slowing, helped amp up volatility during October. Yields on long-term bonds rose as prices fell, with the yield on 10-year Treasuries climbing about 8 basis points on the last day of the month.

By the close of trading on October 31, the price of crude oil (WT) was $64.95 per barrel, down from the September 28 price of $73.53 per barrel. The national average retail regular gasoline price was $2.811 per gallon on October 29, down from the September 24 selling price of $2.844 but $0.356 more than a year ago. The price of gold rose by the end of August, closing at $1,216.80 on the last trading day of the month, up from its price of $1,195.20 at the end of September.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Month's Economic News

- Employment: Total employment rose by 134,000 in September after adding 270,000 (revised) new jobs in August. The average monthly gain over the last 12 months is 201,000. Notable employment gains for the month occurred in professional and business services (54,000), health care (26,000), transportation and warehousing (24,000), and construction (23,000). The unemployment rate declined 0.2 percentage point to 3.7% in September. The number of unemployed persons fell to 6.0 million. The labor participation rate remained at 62.7%. The employment-population ratio increased 0.1 percentage point to 60.4%. The average workweek in September was unchanged at 34.5 hours. Average hourly earnings increased by $0.08 to $27.24. Over the last 12 months, average hourly earnings have risen $0.73, or 2.8%.

-

FOMC/interest rates: The Federal Open Market Committee did not meet in October. The next meeting is scheduled for November 7-8.

-

GDP/budget: The initial, or advance, estimate of the third-quarter gross domestic product showed the economy expanded at an annualized rate of 3.5%, according to the Bureau of Economic Analysis. The second-quarter GDP grew at an annualized rate of 4.2%. According to the report, consumer spending surged, increasing at a rate of 4.0% (3.8% in the second quarter). The net exports deficit expanded by $99.0 billion, pulling the GDP down by 1.8%. There was a $119 billion surplus in September. Nevertheless, the government deficit ended the fiscal year at roughly $779 billion — an increase of almost $113 billion, or 17%, over fiscal year 2017. For fiscal 2018, individual tax receipts were $96.4 billion higher than 2017 receipts, while corporate tax receipts fell by $92.3 billion.

-

Inflation/consumer spending: Inflationary pressures continue to creep along, while consumer spending continues to be strong. According to the Personal Income and Outlays report, prices for consumer goods and services rose only 0.1% in September, the same mark reached in August. Core consumer prices (excluding food and energy), a tracker of inflationary trends, rose 0.2%. Core prices have increased 2.0% over the last 12 months — right on the Federal Reserve's target for inflation. Consumer spending climbed 0.4% in September after jumping 0.5% (revised) in August. Consumer income (pre-tax and after-tax) rose 0.2%, respectively, for the month.

-

The Consumer Price Index rose 0.1% in September after increasing 0.2% in August. Over the last 12 months ended in September, consumer prices are up 2.3%. Core prices, which exclude food and energy, climbed 0.1% for the month and are up 2.2% over the last 12 months.

-

According to the Producer Price Index, the prices companies receive for goods and services actually jumped 0.2% in September, the same increase as in August (revised). Producer prices have increased 2.6% over the 12 months ended in September. Prices less food and energy also gained 0.2% in September, and are up 2.5% over the last 12 months.

-

Housing: New home sales fell 5.5% in September and are down 13.2% from the September 2017 estimate. The median sales price of new houses sold in September was $320,000 ($320,200 in August). The September average sales price was $377,200 ($388,400 in August). Inventory rose to an estimated 7.1-month supply, slightly behind August's 6.1 months. Sales of existing homes dropped in September by 3.4% from August. Year-over-year, existing home sales are down 4.1%. The September median price for existing homes was $258,100, down from $264,800 in August. However, existing home prices are up 4.2% from September 2017. Total housing inventory for existing homes for sale last month was 1.88 million, down from August's 1.91 million. Unsold inventory is at a 4.4-month supply at the current sales pace.

-

Manufacturing: Industrial production advanced 0.3% in September, its fourth consecutive monthly increase. For the year, industrial production has advanced 5.1%. Manufacturing output increased 0.2% following a 0.2% increase in August. The output of utilities was unchanged from August, but is up 5.4% for the year. The index for mining continued to show strong gains, climbing 0.5% in September and 13.4% over the last 12 months. New orders for long-lasting durable goods, up three of the past four months, grew 0.8% in September, following a 4.6% August increase. Most of the monthly gain was attributable to robust orders for defense aircraft. Durable goods orders excluding transportation inched up a scant 0.1%.

-

Imports and exports: The advance report on international trade in goods revealed that the trade gap expanded in September to $76.0 billion. The deficit for August was $75.5 billion. September exports of goods increased 1.8%, while imports rose 1.5%. Prices for imported goods grew by 0.5% in September after dropping 0.4% in August. Export prices were unchanged for the month. Over the last 12 months ended in September, import prices are up 3.5%, while export prices have advanced 2.7%.

-

International markets: Major investor sell-offs in October have cost global stock and bond markets about $5 trillion in value. The Chinese yuan fell to its weakest price since May 2008, hit by an economic tailspin that's been exacerbated by U.S. tariffs. The United Kingdom announced that it would be the first industrialized nation to tax digital services, with other countries soon to follow. Angela Merkel announced that she will step down as German chancellor when her mandate ends in 2021.

-

Consumer confidence: Consumer confidence, as measured by The Conference Board Consumer Confidence Index®, rose in October, following a modest improvement in September. Consumer confidence increased in current business and labor market conditions. Consumers also looked favorably on short-term income, business, and labor market conditions.

Eye on the Month Ahead

Investors will be looking for stocks to rebound in November following a treacherous October. November's midterm elections likely will play a big role in the stock market in particular, and in the economy in general.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e. wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indices listed are unmanaged and are not available for direct investment.