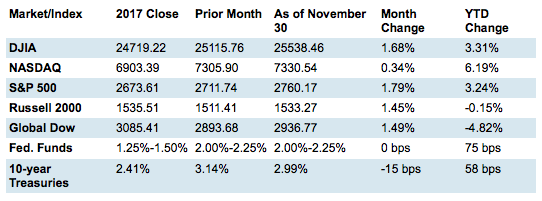

November proved to be a very volatile month for stocks. By the third week of the month, the benchmark indexes listed here had given back just about all of the gains accumulated during the year. However, a spurt during the last week of November helped push stocks higher by the end of the month.

Each of the indexes listed here outperformed their October end-of-the-month closing values, led by the large caps of the S&P 500 and the Dow, followed by the Global Dow and the small caps of the Russell 2000. The technology stocks of the Nasdaq edged higher by the close of November, and that index still maintains a sizeable lead year-to-date among the indexes listed here.

Nevertheless, investors head into the last month of the year anxiously, as fears of a slowing economy and growing international trade tensions will likely temper expectations for steady stock gains moving forward. Energy stocks have been hit by falling oil prices, and the yield on 10-year Treasuries fell below 3.0% as bond prices rose after the Federal Reserve chairman intimated that interest rates may not be increasing as aggressively as previously thought.

By the close of trading on November 30, the price of crude oil (WTI) was $50.72 per barrel, down from the October 31 price of $64.95 per barrel. The national average retail regular gasoline price was $2.539 per gallon on November 26, down from the October 29 selling price of $2.811 and only $0.006 more than a year ago. The price of gold rose by the end of November, closing at $1,227.80 on the last trading day of the month, up from its price of $1,220.80 at the end of October.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Month's Economic News

- Employment: Total employment rose by 250,000 in October after adding 180,000 (revised) new jobs in September. The average monthly employment gain over the last 12 months is 211,000. Notable employment increases for the month occurred in leisure and hospitality (42,000), professional and business services (35,000), manufacturing (32,000), health care (36,000), transportation and warehousing (25,000), and construction (30,000). The unemployment rate remained at 3.7% in October. The number of unemployed persons was little changed at 6.1 million. Over the year, the unemployment rate and the number of unemployed persons declined by 0.4 percentage point and 449,000, respectively. The labor participation rate rose 0.2 percentage point to 62.9%. The employment-population ratio increased 0.2 percentage point to 60.6%. The average workweek increased 0.1 hour to 34.5 hours in October. Average hourly earnings increased by $0.05 to $27.30. Over the last 12 months, average hourly earnings have risen $0.83, or 3.1%.

-

FOMC/interest rates: The Federal Open Market Committee met in November but declined to raise interest rates, which remained at their current 2.00%-2.25% range. The next meeting is scheduled for December 18-19. Following its September meeting, the Fed forecast one more rate hike this year. However, it may push that rate change into 2019, unless it determines that economic expansion and/or inflation are ratcheting up too fast.

-

GDP/budget: According to the second estimate, the third-quarter gross domestic product increased at an annual rate of 3.5%. The second-quarter GDP grew at an annualized rate of 4.2%. The economy has expanded for nine consecutive years, the second longest such streak on record. Spending by consumers and state and local governments receded in the third quarter. Business investment and inventories are up, likely due to companies trying to stockpile in anticipation of tariffs driving import prices higher. October is the first month of fiscal 2019 for the federal government. There was a $100.5 billion deficit in October, with government receipts totaling $252.7 billion, offset by $353.2 billion in expenses. The biggest expenditures in October were for Social Security ($84 billion), national defense ($69 billion), and Medicare ($53 billion). In October the government collected $129 billion in individual income taxes, but only $8 billion in corporate income taxes.

-

Inflation/consumer spending: Inflationary pressures were subdued in October, while consumer spending was strong. According to the Personal Income and Outlays report, prices for consumer goods and services rose only 0.2% in October following a 0.1% increase in September. Core consumer prices (excluding food and energy), a tracker of inflationary trends, increased 0.1%. Core prices have increased 1.8% over the 12 months ended in October — 0.2 percentage point below the Federal Reserve's target for inflation. Consumer spending climbed 0.6% in October after jumping 0.2% (revised) in September. Consumer income (both pre-tax and after-tax) rose 0.5%, respectively, for the month.

-

The Consumer Price Index rose 0.3% in October after increasing 0.1% in September. Over the last 12 months ended in October, consumer prices are up 2.5%. Core prices, which exclude food and energy, climbed 0.2% for the month and are up 2.1% over the last 12 months.

-

According to the Producer Price Index, the prices companies received for goods and services jumped 0.6% in October following a 0.2% increase in September. Producer prices have increased 2.8% over the 12 months ended in October. Prices less food and energy gained 0.5% in October, and are up 2.6% over the last 12 months.

-

Housing: New home sales fell 8.9% in October after declining 1.0% in September (revised) and are down 12.0% from the October 2017 estimate. The median sales price of new houses sold in October was $309,700 ($321,300 in September). The October average sales price was $395,000 ($379,000 in September). Inventory rose to an estimated 7.4-month supply, slightly ahead of September's 7.1 months. Following six straight months of decreases, sales of existing homes increased 1.4% in October. Year-over-year, existing home sales are down 5.1%. The October median price for existing homes was $255,400, down from $258,100 in September. However, existing home prices are up 3.8% from October 2017. Total housing inventory for existing homes for sale fell from 1.88 million in September to 1.85 million in October, rendering a 4.3-month supply at the current sales pace.

-

Manufacturing: The manufacturing sector slowed in October. Industrial production edged up 0.1% following a 0.3% advance in September. For the 12 months ended in October, industrial production has advanced 4.1% — down from the 5.1% annual gain in September. Manufacturing output increased 0.3% following a 0.2% increase in September. The indexes for mining and for utilities declined 0.3% and 0.5%, respectively. New orders for long-lasting durable goods fell 4.4% in October following a revised September report that moved from an 0.8% gain to 0.1% a decline. Durable goods orders excluding transportation inched up a scant 0.1%.

-

Imports and exports: The advance report on international trade in goods revealed that the trade gap expanded in October (the first month of fiscal 2019) to $77.2 billion — up from $76.3 billion in September. Compared to the prior month, October exports of goods decreased $0.8 billion to $140.5 billion, while imports rose $0.2 billion to $217.8 billion. Prices for imported goods grew by 0.5% in October after climbing 0.2% (revised) in September. Export prices increased 0.4% in October following no price change in September. Over the last 12 months ended in October, import prices are up 3.5%, while export prices have advanced 3.1%.

-

International markets: The British pound remained at historically weak levels, influenced by the ongoing Brexit ordeal. The next major action in the ongoing drama involving the United Kingdom's withdrawal from the European Union occurs on December 11, when the UK Parliament is set to vote on the proposed agreement to leave the EU. Analysts suggest that parliamentary approval of the deal is tenuous at best. A "no" vote could lead to several possible outcomes. On the trade front, heading into a meeting between President Trump with President Xi Jinping of China at the Group of 20 (G20) summit, President Trump threatened additional tariffs on Chinese imports if the meeting did not produce a favorable outcome for the United States.

-

Consumer confidence: The Conference Board Consumer Confidence Index® declined in November, following an improvement in October. While consumers' assessment of current business and labor market conditions improved slightly, consumers' short-term outlook for income, business, and labor market conditions waned.

Eye on the Month Ahead

December will close what has been a tumultuous year for the stock market and the economy. Manufacturing, durable goods orders, and real estate are sectors that could use a push as 2018 closes. The employment sector should add more new jobs in December, although wage inflation isn't expected to surge. Entering the holiday season, consumer spending, which has been strong, should advance further, while prices are expected to remain stable.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e. wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indices listed are unmanaged and are not available for direct investment.